The AI Go-to-Market Gap is Growing

Two years ago, the loudest argument in software was whether AI would replace salespeople. This year, we asked 111 founders how AI had actually impacted how they sell.

Sentiment is up. Measured productivity is up. The “AI = layoffs” narrative is mostly wrong. And the performance gap between the best and worst GTM teams has become an AI-deployment gap. Visit our 2026 GTM Survey Dashboard for full results.

1. Founders are *more* confident about AI, not less.

Median sentiment about 2026: 7.0, up from 6.7 in 2024.

If you were expecting an "AI disillusionment" cycle, the data doesn't show one. 63% of founders call AI very useful or transformational. Only 6% call it overhyped or net negative.

2. Expectations for AI’s productivity impact have outrun measurement.

In 2024, when we asked founders a single question about AI’s productivity contribution, the median answer was 10% (with 37% observing zero gain).

In 2026 we split the question. The median founder perceives a 28% productivity gain — but the median measured gain is 10%, unchanged from 2024.

Measurement hasn’t moved. Perceptions have. The new story isn’t convergence — it’s an 18-point gap between what founders feel AI is delivering and what they can actually count.

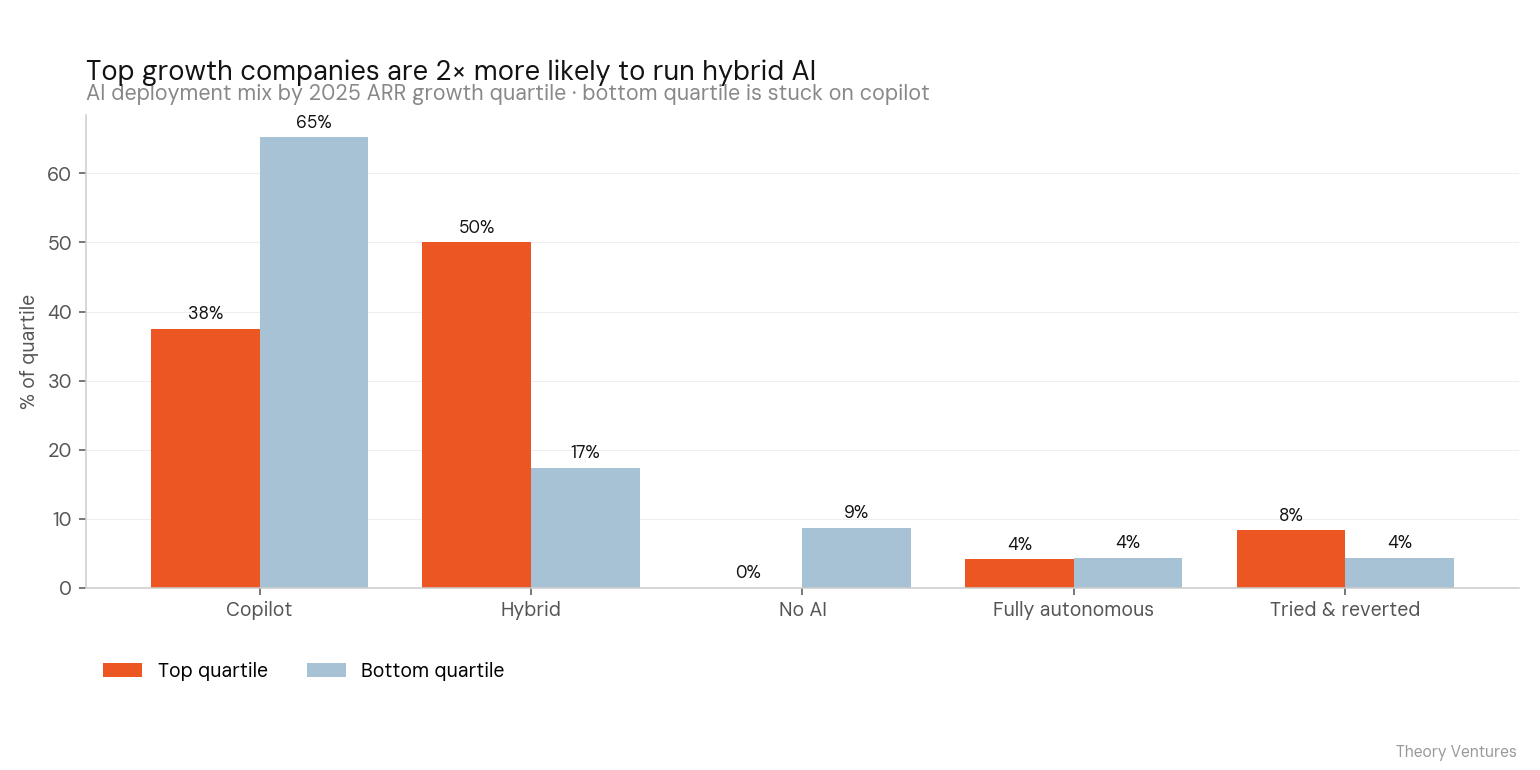

3. The top and bottom of the market are pulling apart, and the growth gap can be attributed to AI.

Split respondents into top and bottom quartiles by 2025 ARR growth:

The top quartile posts an efficiency score more than 2× the bottom (90 vs 42), spends roughly 4× more on AI tooling per month, and is twice as likely to run hybrid AI rather than pure copilot.

Every company is leveraging AI in some way, and the ones who’ve built sophisticated AI deployments are pulling away from the ones who haven’t.

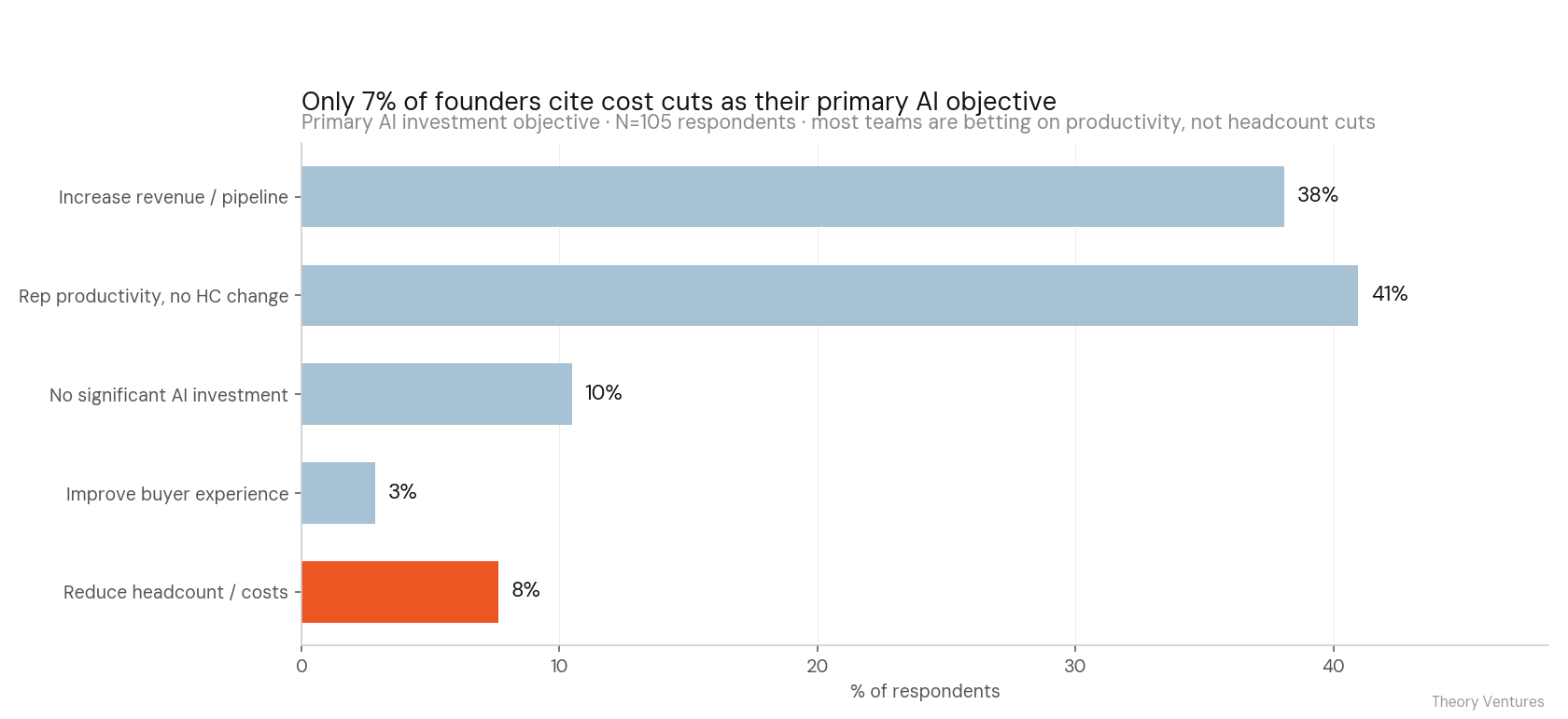

4. The "AI as layoff tool" narrative is mostly wrong.

When asked about their primary AI investment objective, our respondents shared that:

- 41% — Improve rep productivity without changing headcount

- 39% — Increase revenue / pipeline

- 10% — Haven't made a significant AI investment

- 7% — Reduce headcount / costs

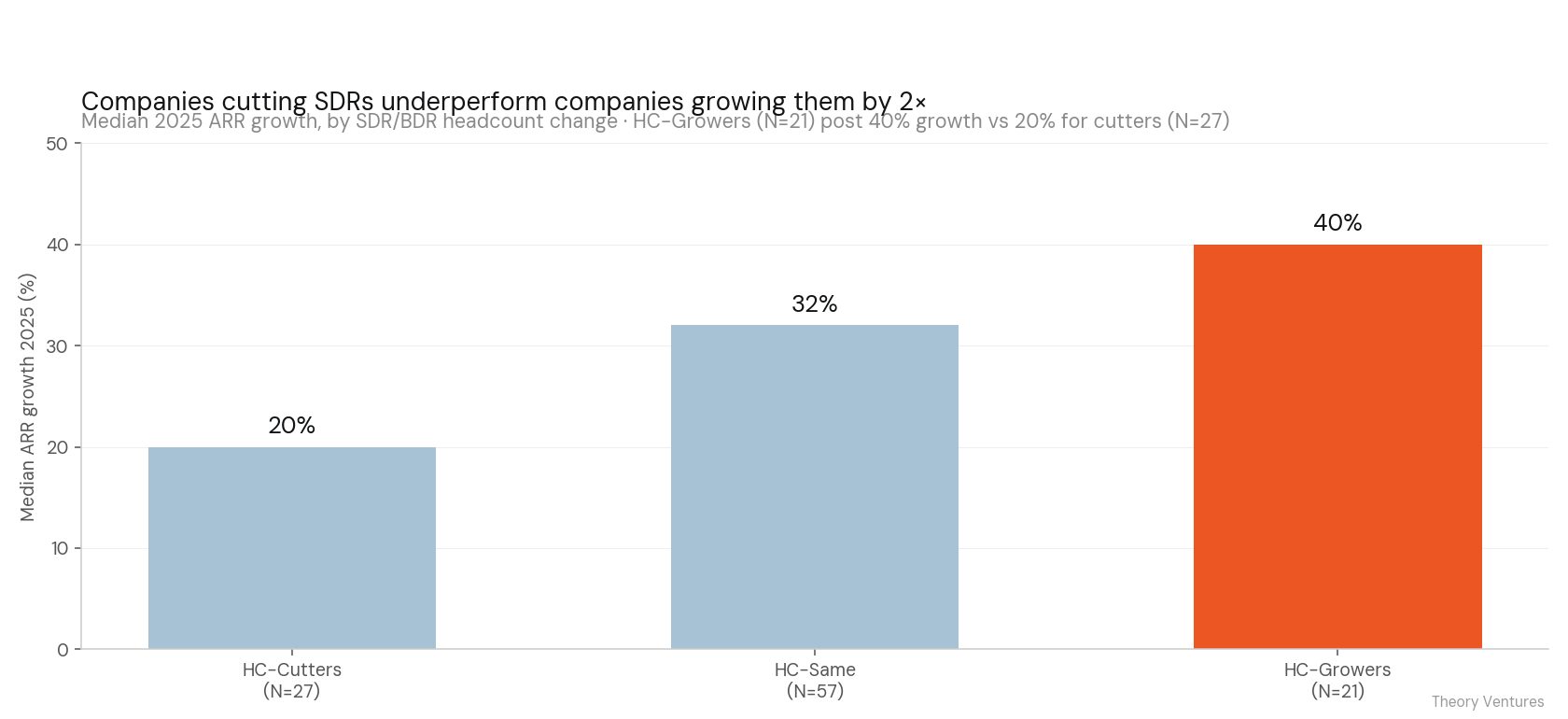

Only 7% of founders frame AI as a cost-cut play. And the companies cutting SDRs aren't outperforming; they're underperforming. Median ARR growth for HC-cutters is 20%; for HC-growers, 40%.

The companies winning are adding SDRs and leaning on AI to make them more productive. The companies cutting are doing so because their growth has stalled.

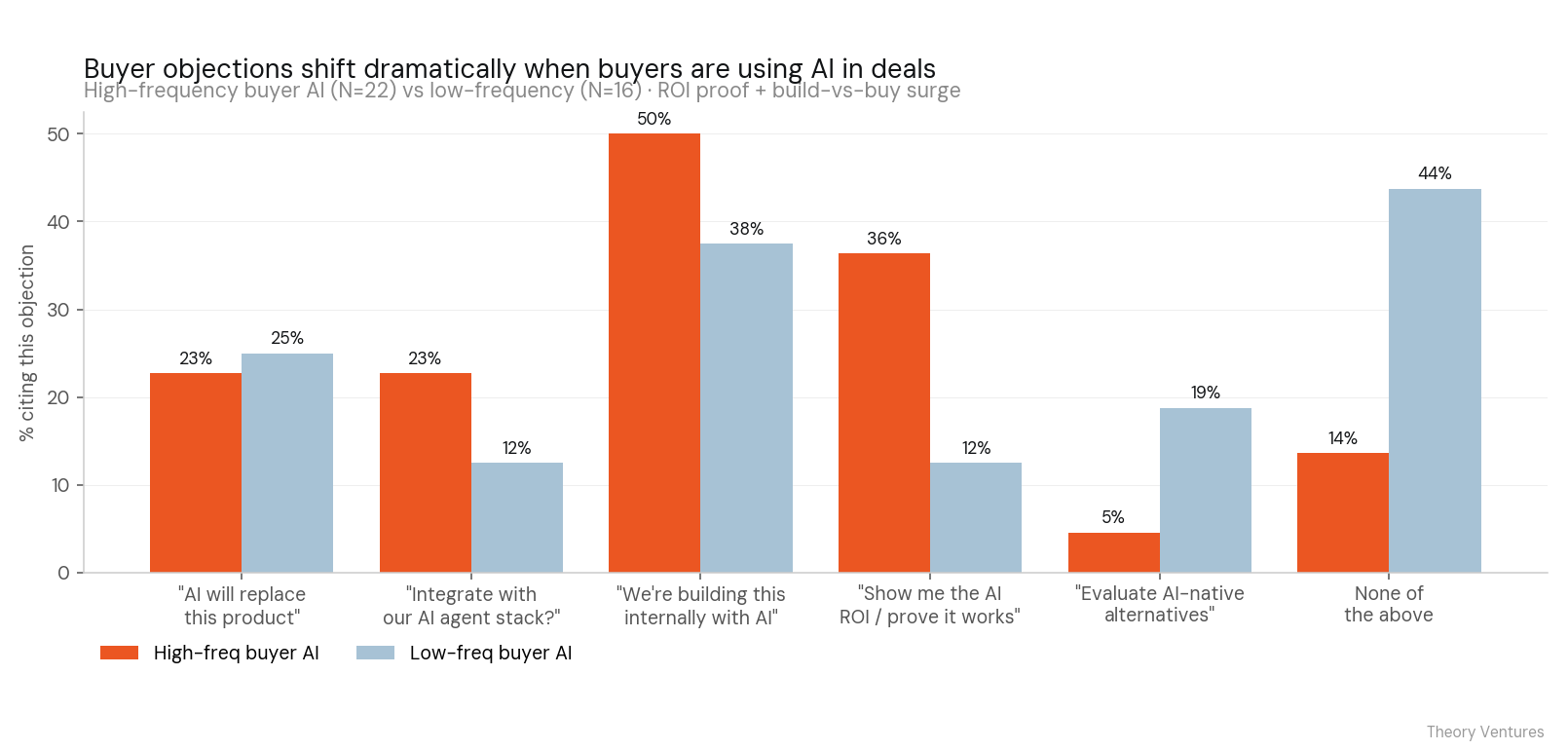

5. Buyer AI doesn't slow deals, but it does change the objections.

We expected buyer-side AI — AI-generated RFPs, automated evaluations — to lengthen sales cycles. It didn't. Cycle change medians are 0% across every level of buyer AI usage.

But it did reshape objections:

When buyers use AI in 25%+ of deals, "show me the AI ROI" goes from 0% to 36% of objections. "We're building this internally with AI" goes from 38% to 50%. But the fear that AI will replace the product actually drops from 31% to 23%. Once buyers have used AI themselves, they become less worried about it as an existential threat to vendors.

If you sell to AI-fluent buyers, your most important assets are now (1) measurable ROI proof and (2) a credible integration story.

What We'd watch in 2027

A few open questions this survey raised:

- Outcome-based pricing sits at 12%. Will it double?

- "Tried autonomous, reverted" is a 4% cohort today. Will it grow?

- Will the top/bottom efficiency gap (90 vs 42) become structural?

- Will buyer AI use cross 50%? Today only 22% of founders report encountering it often (defined as, in over 25% of their deals).

Full results, all 25 questions, every chart: 2026 GTM Survey dashboard

111 founders, fielded Q2 2026. Software/SaaS heavy (78%), mid-market/enterprise heavy (81%). 14 questions carried forward from the 2022, 2023, and 2024 surveys for longitudinal comparison.